Startup exits are usually discussed from the perspective of founders and investors. When a company is sold, the focus is often on the purchase price, the founders’ returns, and what the deal means for the startup ecosystem. But employees are also part of the story. If startup work involves lower early pay or higher career risk, then one important question is whether employees share in the upside when the company succeeds.

In this analysis, we look at what happens to startup employees’ income before and after an exit. Here, an exit event means that a majority stake in the startup is sold. The analysis uses register-based data on startup employees in Finland, and founders are excluded from the dataset. This means the focus is on employees rather than owner-founders.

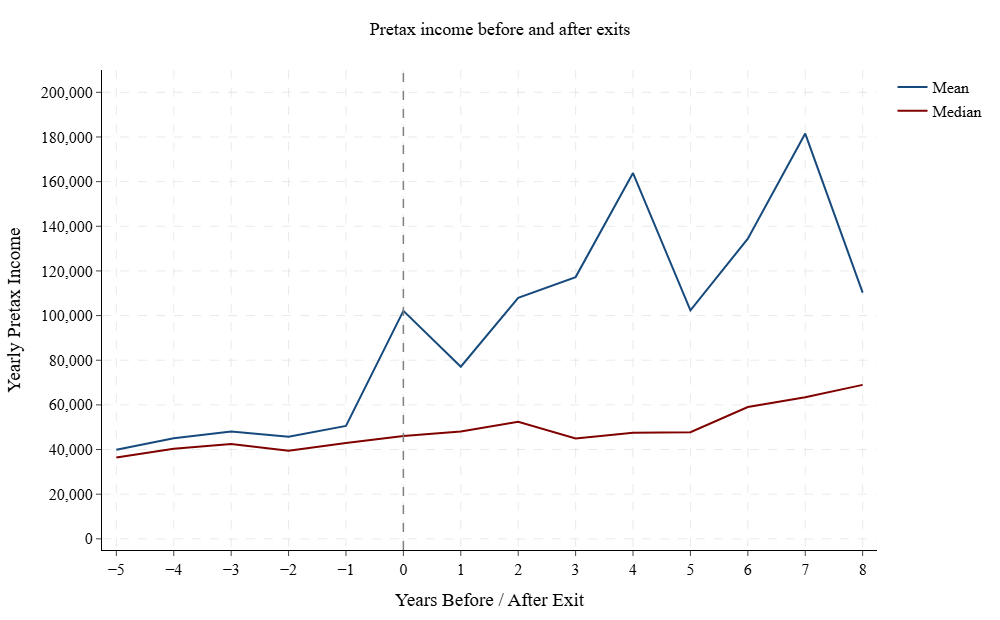

Figure 1 shows how mean and median pretax income evolve for startup employees before and after the exit event. Pretax income includes both earned income and capital gains, and therefore captures wages and salaries as well as income from shares, stock options, and other equity-related gains. The figure indicates a clear break around the exit event. Mean pretax income rises sharply at the time of exit and, on average, continues to increase rapidly in the years that follow. This suggests that the income effects of an exit are not confined to a one-time spike, but may persist beyond the year in which the majority stake is sold.

Fig 1: Mean and median pretax income 5 years before and 8 years after a startup exit (Finnish Startup Community, Statistics Finland, 2026)

The changes in the median pretax income tells a more cautious story. Unlike the mean, median pretax income does not spike at the exit event. Instead, it increases more gradually over time. This difference between the mean and the median is central to interpreting the figure. The sharp increase in average income appears to be driven by large gains among a smaller group of employees, rather than by an equally large increase for the typical worker.

This pattern is consistent with the role of equity-related income in startup compensation. Some employees may receive substantial gains from shares, stock options, or other ownership-linked rewards when the majority stake is sold. At the same time, many employees may receive more modest gains, or no direct equity-related payout at all. In other words, the exit appears to create significant financial upside for employees, but the largest gains are likely concentrated among a limited group of workers.

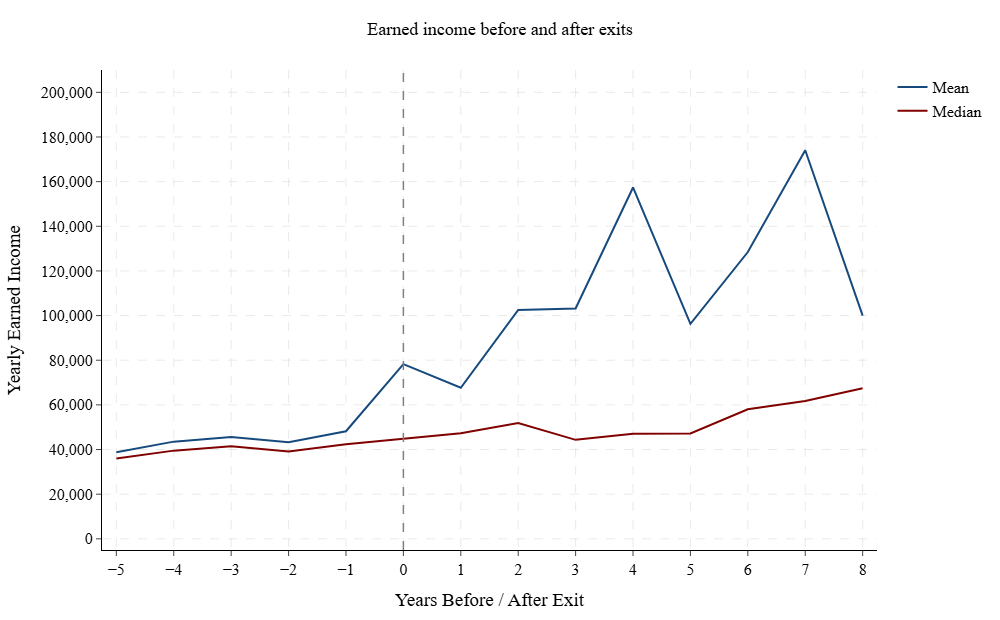

To better understand the role of labor income, Figure 2 shows the mean and median earned income of startup employees before and after the exit event. Earned income excludes capital gains and therefore focuses more directly on wages, salaries, bonuses, and other income from work.

Figure 2 shows that earned income also increases after the exit event, but the pattern is less pronounced than for pretax income. Mean earned income rises around the time of exit and continues to increase in the following years. This suggests that employees may benefit after an exit not only through capital gains, but also through higher labor income, for example through bonuses, career progression, or transitions into better-paid roles.

Fig 2: Mean and median earned income 5 years before and 8years after a startup exit (Finnish Startup Community, Statistics Finland, 2026)

However, as in Figure 1, the difference between the mean and the median is important. Median earned income increases more gradually and remains below the mean throughout the post-exit period. This suggests that the gains in earned income are also unevenly distributed across employees. The increase is not driven solely by capital gains, but the strongest income growth still appears to be concentrated among a smaller group of workers.

Taken together, our analysis shows a back-loaded compensation model in startups. Before the exit, employees’ income is relatively stable. The large financial rewards appear mainly after the company succeeds and a majority stake is sold. This helps explain why equity compensation is central to startup labor markets. For employees, the potential upside may not show up in annual salary before the exit, but it can become visible when the company is sold.

At the same time, the results also show that the upside is uneven. The sharp rise in mean income compared with the more moderate rise in median income suggests that the largest gains go to a smaller group of employees. This does not mean that other employees do not benefit, but it does mean that the average can give an overly optimistic picture of the typical employee experience.

These findings lead to some interesting thoughts about how the startup ecosystem works. For startups to attract talent, employees need a fair chance to benefit from the value they help create. This is why the taxation of stock options and capital gains is such a relevant topic. If these rewards are taxed heavily or are difficult to use, startup jobs might look less attractive compared to more stable roles in established firms.

Beyond individual rewards, exit benefits include both one-time gains and long-term salary growth. We can hypothesize that this financial upside acts as a spark for the whole community. For example, successful workers might use the money they receive in exits to become angel investors. By doing this, they help keep both money and skills recycling back into the next generation of startups.

The key takeaway is that when a majority stake in a startup is sold, employees’ pretax income increases rapidly. However, the comparison between mean and median income shows that the largest gains are concentrated among a smaller group. Startup exits can benefit employees, but the benefits are not evenly distributed.

About the data used in this analysis

This analysis is based on Finnish administrative register data on startup employees. We identify 161 startup exit events, where an exit is defined as the sale of a majority stake in the company. These firms employed 3,801 people in the year of the exit.

Founders are excluded from the dataset, which means the analysis focuses on employees rather than owner-founders. The income measures are based on individual-level register data. Pretax income includes both earned income and capital gains, allowing the analysis to capture wages and salaries as well as income from shares, stock options, and other equity-related gains. Earned income is examined separately to distinguish changes in labor income from capital gains around the exit event.

The employee group is not fixed over time. Employees can join and leave the companies before and after the exit, which means that the composition of employees may change across the years shown in the figures. The results should therefore be interpreted as describing the income development of employees observed around startup exits, rather than the income path of one unchanged group of workers.

It is also important to note that not all firms remain in the data for the full post-exit period. After an exit, some firms may disappear from the dataset relatively soon. This can happen because exits may involve mergers, acquisitions, changes in legal structure, or other corporate arrangements, rather than the firm continuing as a separate entity in the same form.

To ensure the reliability of the analysis and maintain a sufficient sample size of firms, the observation period is capped at eight years post-exit. Beyond this point, the number of participating firms decreases significantly, which could distort conclusions based on mean and median figures.

The analysis is descriptive: it follows how employees’ income develops before and after an exit, but it does not by itself prove that the exit caused all observed income changes.